It is finally time to get serious about flood insurance. New flood maps for Key West and the Monroe County are going to raise premiums nearly across the board. Many premiums will still be government subsidized and therefore lower than premiums that would be charged by private sector insurance companies. But many new premiums will be higher and will continue upward until they meet full premium requirement. And so, what are your options to keep premiums as low as possible for as long as possible? There are multiple solutions. Letters of Map Change. Mitigation. Buyout. Let's take a look.

How Did We Get Here?

A brief review of the previous nine articles -

- Is Your Flood Insurance Going Up - Part IX (June 2019) - A review of the three largest roadblocks to viable flood insurance; affordability, mapping and mitigation.

- Is Your Flood Insurance Going Up - Part VIII (May 2018) - New elements of the projected bill including "inland storm surge", new mapping techniques and grandfathering.

- Is Your Flood Insurance Going Up - Part VII (August 2017) - Review of the new, bipartisan Senate bill called "The Sustainable, Affordable, Fair and Efficient National Flood Insurance Program Reauthorization Act (SAFE NFIP) 2017.

- Is your Flood Insurance Going Up - Part VI (June 2016) - Update of the FEMA RiskMap mapping project begun in 2013.

- Is Your Flood Insurance Going Up - Part V (July 2014) - Details of the FEMA mapping effort for the Keys and South Florida including an extensive Outreach Program.

- Is Your Flood Insurance Going Up - Part IV (March 2014) - Recap of the March 2014 Homeowners Flood Insurance Affordability Act (HFIAA).

- Is Your Flood Insurance Going Up - Part III (October 2013) - Realization by politicians, including a co-author of flood insurance legislation called the Biggerts Waters Insurance Reform Act of 2012 (BW-12), that BW-12 was causing the consumer more harm than good, aka "unintended consequences".

- Is Your Flood Insurance Going Up - Part II (September 2013) - Treatment of historic buildings, second homes, businesses and no more exemptions under BW-12.

- Is Your Flood Insurance Going Up - Part I (January 2013) - Flood insurance rate changes and their justifications according to BW-12; i.e., refund the bankrupt NFIP.

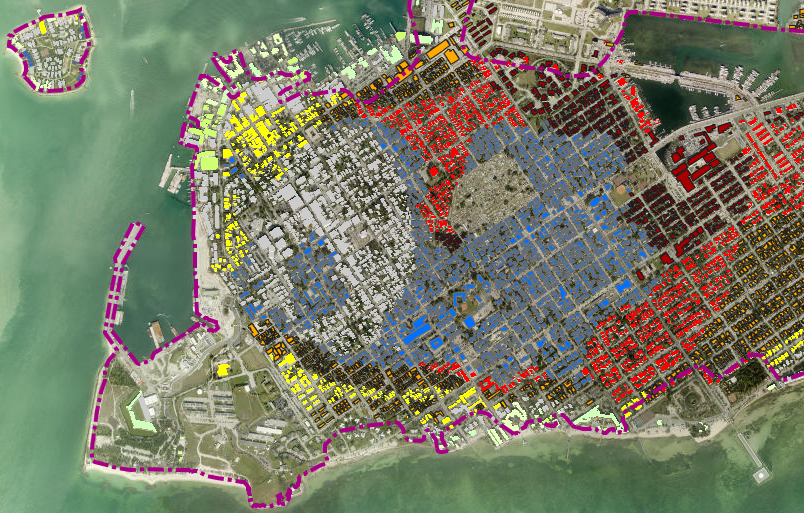

What flood zone is my property?

It is very easy to locate your property in the new proposed Draft Flood Map.

- Select this link to the FEMA Draft Flood Maps for Key West.

- In the Top Left Corner type your address in the block labeled "Find address or place".

- The address is shown on the Draft map with a New Flood Level Impacts color code on the right side of the screen. These color/number codes tell you that you have gained or lost flood elevation.

What do these color/number codes really tell you? Keep it simple -

For instance, If your property has a New Flood Level Impacts color of orange with the number 2 next to it that means you now have a new risk of 2 additional feet of flooding. BE ADVISED - these color codes and numbers are for the AREA in which your property is located. Only an Elevation Certificate can determine the actual height you property is above or below Base Flood Elevation (BFE).

What Do I Do?

First things first. If you have been living without flood insurance, get flood insurance ASAP. Many people who have been living in the X-Flood Zone .2 percent annual chance flood hazard, aka X Shaded, have likely not been carrying flood insurance. X Shaded, affecting 2000+ predominantly Old Town homeowners, is going away in Key West. Flood insurance will become a necessity. Therefore:

- Get a flood policy NOW.

- Having a flood policy before implementation of the new flood maps will prevent your premiums from snapping up to the full value of the new AE flood zone.

- Call your insurance agent and request a Preferred Risk Policy. For $400 - $500 you'll have a flood policy that simultaneously safeguards yourself from a big increase when the new flood maps go into effect. If you do not have a flood policy in effect when the new maps are implemented, then you very likely will immediately begin paying full value AE premiums.

Second things second. Get an Elevation Certificate. Before any challenge of any type can be initiated by you regarding your rating or mitigation or premiums or anything, you must have an Elevation Certificate. Most any surveyor can provide. I use Florida Keys Land Survey.

A key component of the new flood maps is the use of a new datum point. Your old Elevation Certificate used the old datum and must be converted to the new datum. No problem. As part of the new flood zone rating and premium process, your insurance agent performs the conversion. Simply stated, if you live in Key West, subtract 1.342' from the elevation of the 1st floor to get the new low point. If you are in Monroe County subtract 1.44'.

Letters of Map Change

The Flood Zone Designation for your area is simply that - for your area. If you believe your house should receive a better rating then FEMA provides, there is a process to request a change in the flood zone designation for your property. This request is know as a Letter of Map Change (LOMC).

There are two types of LOMC:

- Letter of Map Amendment (LOMA)

- Letter of Map Revision Based on Fill (LOMR-F)

LOMA - LOMAs are usually issued because a property has been inadvertently mapped as being in the base floodplain, but is actually on natural high ground above the base flood elevation. There is no fee associated with a LOMA application and review.

LOMR-F - LOMR-F is FEMA's modification of the Designation for the property based on the placement of fill in excess of the existing base floodplain. For FEMA to issue a LOMR-F that modifies the Designation for your property, the entire lot and all structures, both the lowest point on the lot and the lowest floor of all structures, must be at or above the 1-percent-annual-chance flood elevation. There is a fee associated with a LOMR-F request.

Both the LOMA and LOMR-F begin with an Elevation Certificate.

Mitigation

According to the National Institute of Building Sciences, the Benefit Cost Ratio (BCR) for mitigation in Flood prone areas is approximately 7:1; that is, $7 are saved for every $1 spent. Benefits include; reduced property loss, reduced cost of add-on living expenses (having to rent or hotel someplace else), reduced business interruption, fewer casualties and cases of PTSD and lesser insurance payouts

For flood mitigation, the Number 1 Priorities are; Elevation, Land Use and Buyout.

There are two types of mitigation; dry and wet. Wet floodproofing allows floodwaters to enter areas around a home. In contrast, dry floodproofing prevents the entry of floodwaters. For mitigation purposes, dry floodproofing is for commercial property and wet is for residential.

Wet floodproofing is practical only for portions of a house that are not used for living space. In Key West and Monroe County this means elevating a house to a required or desired Flood Protection Elevation (FPE); specifically, Elevating by Abandoning the Lower Enclosed Area or, Elevating on an Open Foundation.

FEMA is budgetted to assist homeowners in the floodproofing of their homes; specifically, elevation as described above. More on this in my next article.

Buyout

The U.S. saves $7 in avoided costs for every $1 spent through the federally funded grants to acquire or demolish flood-prone buildings, aka Buyout.

Owners of properties that have sustained significant flood damage have the option to allow the government to acquire the property through a buyout. FEMA works with state governments to finance this action. The owner receives the fair market value for the property. The property is then demolished, permanently avoiding future damages and allowing the floodplain to absorb more water without damaging other structures.

How is this done? The homeowner makes application to the County which then makes application to the State. FEMA funds the State which transfers financing to the County which transfers financing to the homeonwer. More on this in my next article.

Conclusion

First, the good news - Monroe County has been very successful in driving Monroe County's Community Rating System (CRS) towards a more favorable FEMA CRS Class 5 rating. This rating improvement from Class 6 to Class 5 has saved County policy holders upwards of $19M over the past five years. A CRS Class 4 rating, which will create further savings, will finalize in 2020. Well Done to CRS Consultant Lori Lehr and her team.

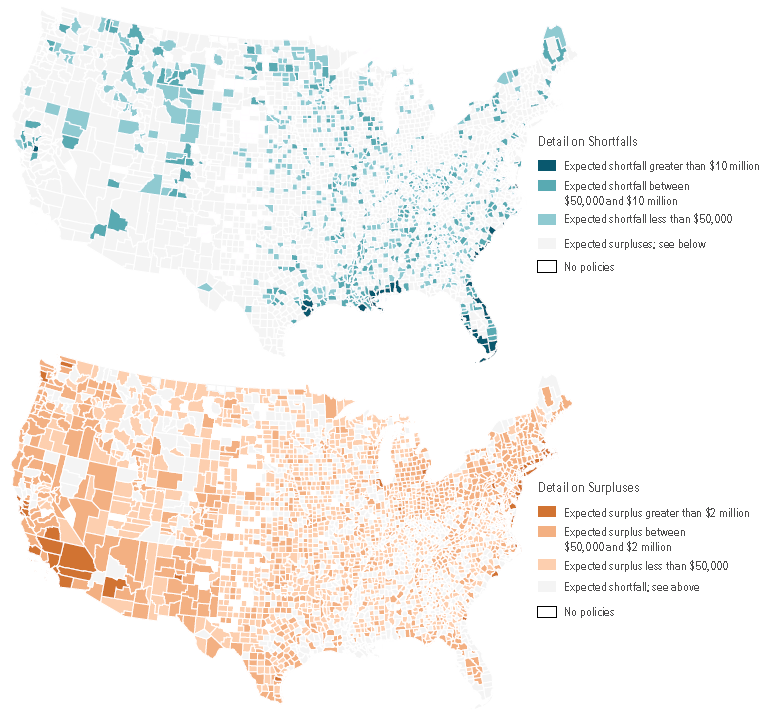

Meanwhile, there is no doubt that the subsidized premiums provided by FEMA through NFIP have fallen short of reliable benefits. As can be seen in the above chart produced by the Congressional Budget Office, NFIP premiums are not actuarily sound. Nationwide, many homeowners pay too much, many too little.

Going forward and without a doubt, NFIP flood insurance premiums are going to rise, reaching a point where private sector insurance companies will enter and write policies specifically tailored to the homeowner. As more private sector companies enter the market and create more and more competitive insurance policies, more and more homeowners will leave NFIP for private coverage.

This is a good thing.

I would very much like to thank Caroline Horn from Fair Insurance Rates in Monroe (FIRM) for her invaluable contributions in helping me write and edit this article. Thank you very much.

If you have any comments or questions, please contact me here.

Good luck!

Additional Resources: